The Essentials of the Corporate Sustainability Reporting Directive (CSRD)

Our AI-powered software and supporting services help companies collect and manage sustainability data and make it easy to meet reporting requirements of the CSRD and EU Taxonomy.

Expertise

Trusted guide in securing ESG compliance

Simplification

Simplifying data collection for effortless compliance

Autonomy

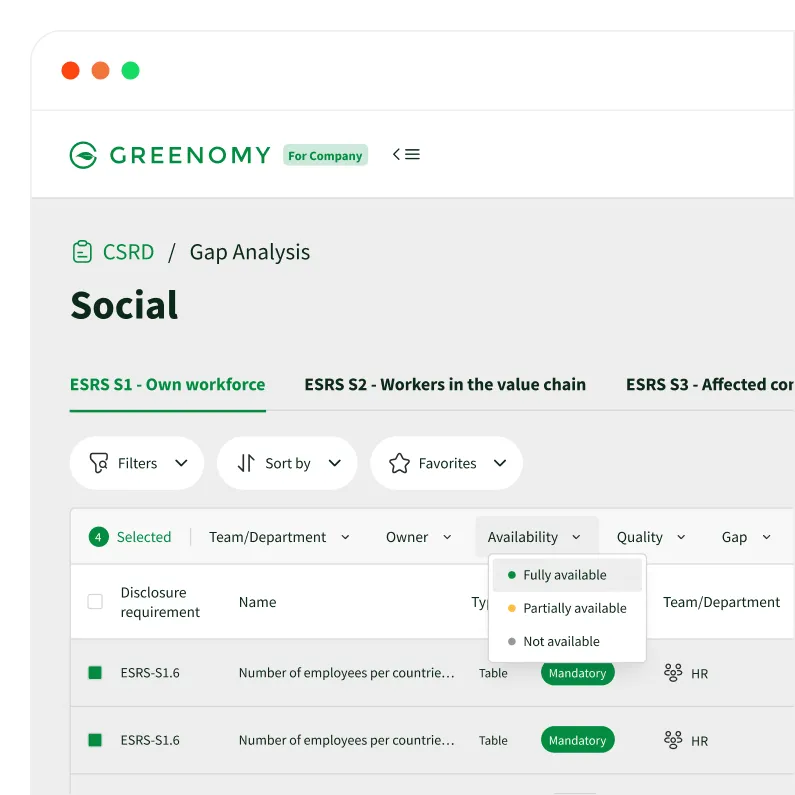

Mastering your ESG reporting, drive strategic changes

Efficiency

Elevating efficiency with AI

Our ESG reporting platform helps you seamlessly navigate the different data requirements for your CSRD and EU Taxonomy reporting. At Greenomy, we simplify your reporting journey allowing you to have more time to drive strategic change.

All your ESG data centralised in one location

Always up to date with the latest regulations

Accelerate your reporting and spend more time on driving impact

Benefit from Artemis, your AI advisor, simplifying ESG requirements

We empower companies to build their capacity through our comprehensive end-to-end solution, prioritising reporting autonomy.

in numbers

customers worldwide

cost savings compared to in-house reporting

faster reporting process

Testimonials

“The partnership allows EcoVadis to enrich its sustainability rating platform with regulatory sustainability reporting requirements, including the EU Taxonomy alignment score. This will broaden EcoVadis’ leader position in the sustainability reporting landscape. The partnership will also allow EcoVadis’ clients to fully comprehend their EU Taxonomy alignment, and to identify actions to be taken to improve their sustainability”

Pierre-François Thaler

Co-founder & co-CEO of EcoVadis

"I find that you give off a feeling of mastery, of control over the subjects that you defend and this gives you a lot of credibility."

Thibaut Alexandre

Head of Sustainable Development at Trafic

"We find Greenomy’s portal user-friendly, it is easy to understand and to use. The Advisory team is professional and gives good advice."

Mateja Bakker

Environmental Manager at IBF Consulting

"The Greenomy solution is easy to use. The step-by-step user guide is effective in generating a complete report in line with investors' expectations and the EU Taxonomy."

Jérôme Chosson

Corporate & Project Finance - Investor Relations, Akuo

“The EU Taxonomy is wildly complicated and near impossible to comply with from a company perspective, but Greenomy helps ease the pain by automating the reporting requirements and providing guidance to companies willing to take the EU Taxonomy seriously. We are grateful for the insights, the understanding and the helping hand Greenomy provided us."

Roel Castelein

Corporate Sustainability Manager, Ziegler Group

“We found Greenomy to be engaging, dedicated, and result-oriented throughout the project. There was close cooperation between us and their team, ensuring that the necessary progress was made and the result was according to expectations. We appreciated the no-nonsense approach of Greenomy, focusing on delivering what we expected. ”

Anton Theunynck

Sustainability Manager at TVH

“Using the Greenomy solution enables user-friendly Sustainability Reporting, and improves, in turn, the ESG Data quality. Specifically, the alignment with European regulation illustrates best practices for companies.”

Quentin Stevenart

Senior Sustainability & Financial Analyst at FIB

"By connecting to the Greenomy infrastructure, we have not only simplified our task as a bank to comply with the new Sustainable Finance regulations but also improved our customers’ access to green financing.”

Rudi Belli

Head of Sustainability at Spuerkeess

“As a solution provider, SCHUFA supports its corporate clients in meeting regulatory requirements and makes processes efficient, digital and convenient. The SCHUFA ESG Solution powered by Greenomy makes it possible to fulfil the disclosure requirements from the EU Taxonomy Regulation and give business partners a clear overview of the sustainability of their business. This is good for business and good for the environment”

Tanja Birkholz

CEO of Schufa Holding AG

greenomy

Your one-stop sustainability reporting SaaS

Greenomy is recognised and certified

.png)

.png)